Inventories, Work in Progress, Contract Costs and IFRS 15

The IFRS Blog is a series of topical issues, common issues and live cases in IFRS Standards and financial reporting.

IFRS 15: Inventories, Work in Progress and Contract Costs

by Steven Zabeti, Accru Felsers, Australia

Capitalised items such as Work In Progress (WIP) requires careful attention because WIP includes partially finished products at various stages of completion and relies on the use of management estimates. Generally, the more raw materials, labour and overhead invested in WIP, the higher the value.

Accounting for WIP affects the balance sheet and the income statement with an overstatement of WIP in the value of inventories at the end of a period resulting in an understatement of costs during the current accounting period.

Client Circumstances

During its local operations, our client capitalises elements of costs on the balance sheet as WIP representing the completion and delivery of each phase of the production process in meeting its contractual obligations with its customers.

During the course of our enquiries, we analysed the method used by local management in quantifying the capitalised value of WIP corresponding to each phase of the production process completed. We also sighted the signed sales contract and obtained supporting documentation regarding the allocation of materials, labour and overheads assigned to the corresponding projects.

The local CFO and MD expressed their confidence that the carrying value of the WIP remains recoverable. However, disruptions with international supply chains from COVID-19 has resulted in unanticipated delays in receiving equipment and raw materials and consequently, delays in completing production projects. Despite these initial setbacks, management demonstrated that the capitalised costs remain recoverable from its customers in the first quarter of the coming financial year.

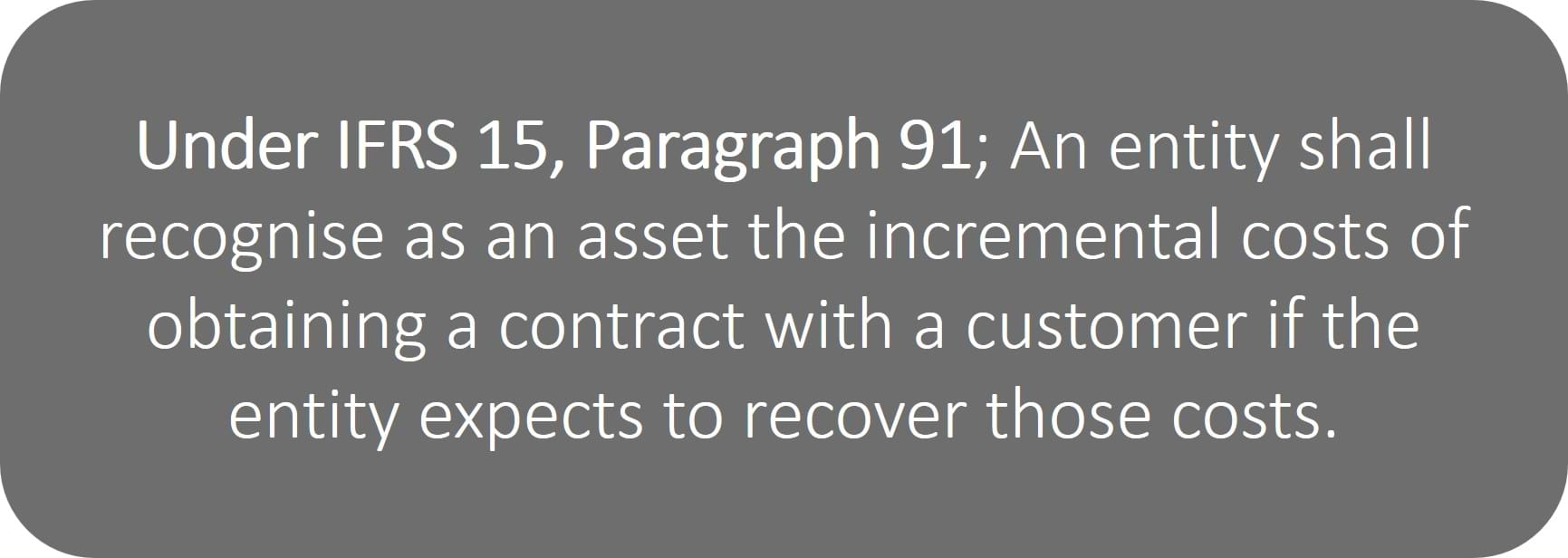

Furthermore, local management have recognised as an asset roughly AUD $2M of incremental costs in obtaining approximately AUD $23M of contracts with customer ACE Australia Pty Ltd that it would not have incurred if the contracts had not been obtained.

Furthermore, local management have recognised as an asset roughly AUD $2M of incremental costs in obtaining approximately AUD $23M of contracts with customer ACE Australia Pty Ltd that it would not have incurred if the contracts had not been obtained.

These capitalised costs of roughly AUD $2M predominantly relate to:

-

Costs directly attributable to contracts and anticipated future contracts with ACE Australia that have been specifically identified;

Costs directly attributable to contracts and anticipated future contracts with ACE Australia that have been specifically identified; - Enhancing future performance obligations with ACE Australia; and

- Costs that are expected to be recovered.

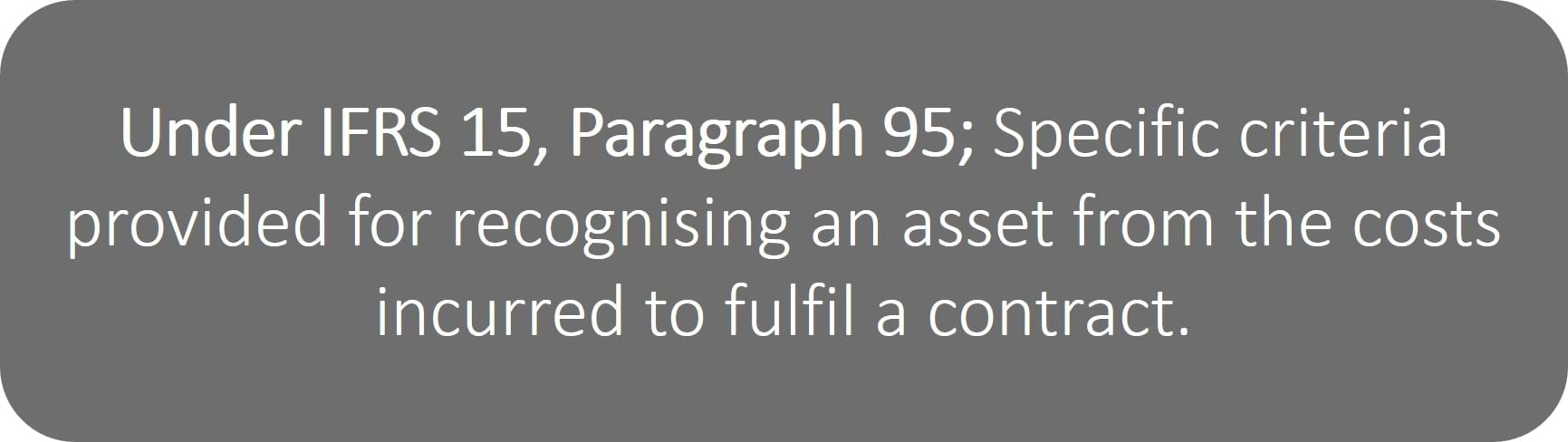

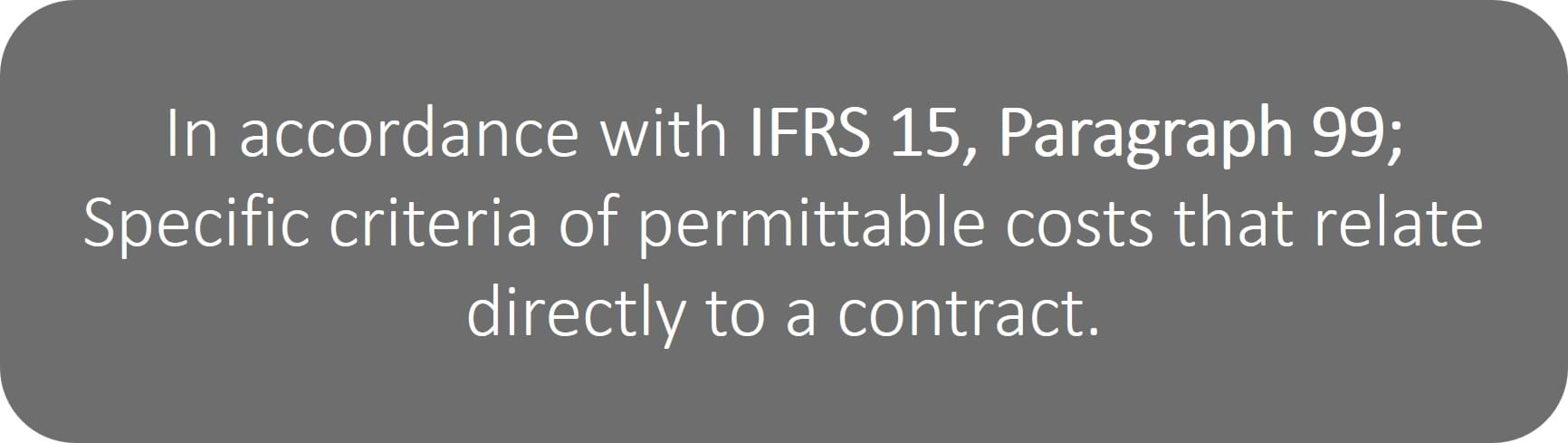

Lastly, these capitalised costs represent:

-

Direct labour and materials that relate directly to contracts and/or anticipated future contracts with ACE Australia;

Direct labour and materials that relate directly to contracts and/or anticipated future contracts with ACE Australia; - Cost allocations relating directly to contracts and contract activities such as contract management and supervision, insurance and depreciation of tools, equipment and right-of-use assets;

- Costs that are explicitly chargeable to ACE Australia under contracts and/or anticipated contracts; and

- Other costs incurred as a result of contractual commitments existing and anticipated.

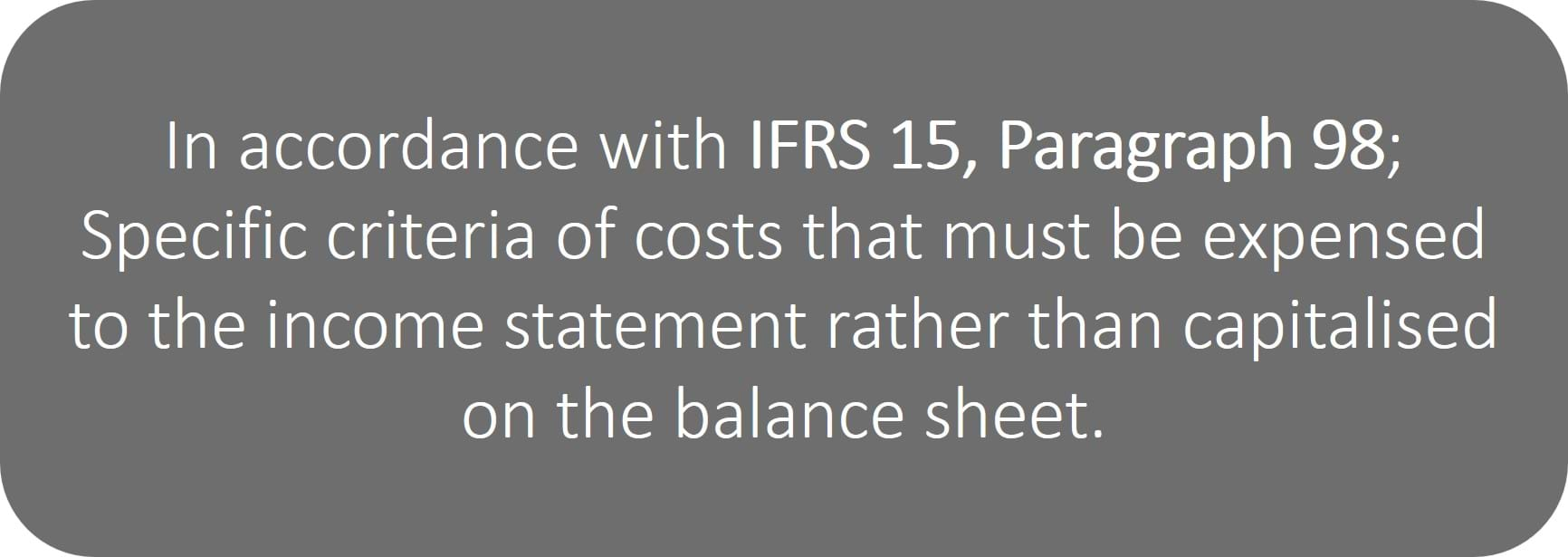

In contrast, the following costs have been recognised as expenses in the income statement when incurred:

-

General and administrative costs;

General and administrative costs; - Costs of wasted materials, labour or other resources to fulfil the contract that were not reflected in the price of the contract;

- Costs that relate to satisfied performance obligations in the contract; and

- Costs for which an entity cannot distinguish whether the costs relate to unsatisfied performance obligations or to satisfied performance obligations.

Please note that entity names have been replaced with pseudonyms to maintain client confidentiality.

MGI Worldwide's Global IFRS specialist have the benefit of continuing day-to-day experience in IFRS. This means that we can bring practical knowledge to IFRS questions raised and help to apply the sometimes complex regulations in a way that minimises the risk of audit adjustments or the detection of accounting errors by national regulators.

If you have any questions about the above or any other aspects of how IFRS may affect your business, please contact a member of the MGI Worldwide CPAAI IFRS Specialist Group or Nicki Lynn, International Business Development Manager [email protected].

MGI Worldwide with CPAAI, is a top 20 ranked global accounting network and association with almost 9,000 professionals, accountants and tax experts in some 400 locations in over 100 countries around the world.