MGI Latin America publishes Spanish language Tax Bulletin

We are excited to announce the publication of MGI Latin America's Spanish language Tax Bulletin. By keeping members informed about the latest tax developments, the region's newsletter aims to help optimise tax strategies, and minimise risks in this dynamic business environment.

We provide below, a summary in English.

What is the profit distribution tax in Latin America and how does it vary from one country to another?

The tax impact is highly relevant when considering an investment project. To support our clients and the entrepreneurial ecosystem in this analysis, we have compiled information from the countries in our region in order to have an overview of the dividend distribution in Latin American countries.

In some countries, the percentage of distribution to resident or non-resident shareholders is a certain percentage, which varies between 0% and 20%. See graphs below.

There are countries where other considerations also come into play, which are also detailed as specific cases below the graphs.

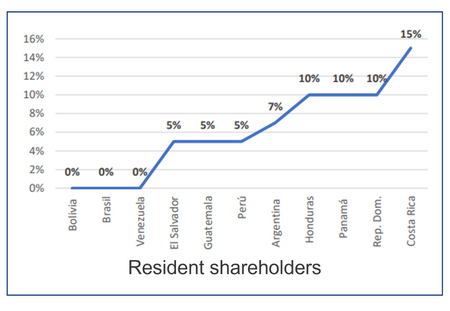

Percentage distribution for resident shareholders

In the case of Colombia, it varies according to: individuals between 0% and 20%; for profits over $10 million the discount is 19%; small shareholders do not pay and large shareholders pay up to 20%.

In the case of Chile, for local resident shareholders the tax is on a progressive scale ranging from 4% to 40%, with deduction of the tax paid by the company.

In Ecuador, after tax, the distribution of dividends to shareholders is given in proportion to their paid-up shares.

In Mexico, a withholding tax of 10% will be applied to dividends from CUFINs generated from 2014 onwards, those from CUFINs prior to that year do not have withholding tax. Legal entities, resident in Mexico, that receive dividends from CUFIN will not be subject to withholding.

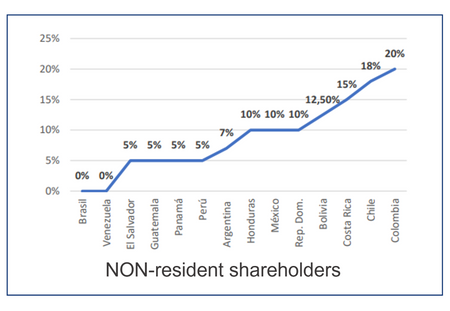

Percentage distribution for non-resident shareholders

In El Salvador, while the tax rate is 5% as shown in the table, when shareholders are domiciled in tax havens, 25% will be withheld.

For Ecuador, as for resident shareholders, after tax, the distribution of dividends to shareholders is given in proportion to their paid-up shares.

In Chile for non-residents the general rate is 35% but the tax paid by the company is deducted, leaving a net rate of 18%.

For Venezuela, profits generated by companies, when distributed as dividends, are never subject to dividend tax. Therefore, there is no percentage for residents or non-residents, it is paid based on the percentage of equity participation or participation quotas.

The FULL Spanish newsletter can be downloaded HERE.

Visit our online directory

MGI Worldwide representatives in Latin America are available to expand on the information provided in this newsletter and to advise you on planning your investments in the region.

Argentina | Bolivia | Brasil | Chile |Colombia | Costa Rica | Ecuador | El Salvador | Guatemala | Honduras | México | Nicaragua | Panama | Peru | Dominican Republic | Venezuela

Find us in the online directory along with full contact details for each of our offices: see here.

MGI Worldwide, is a top 20 ranked global accounting network and association with almost 9,000 professionals, accountants and tax experts in some 400 locations in over 100 countries around the world.